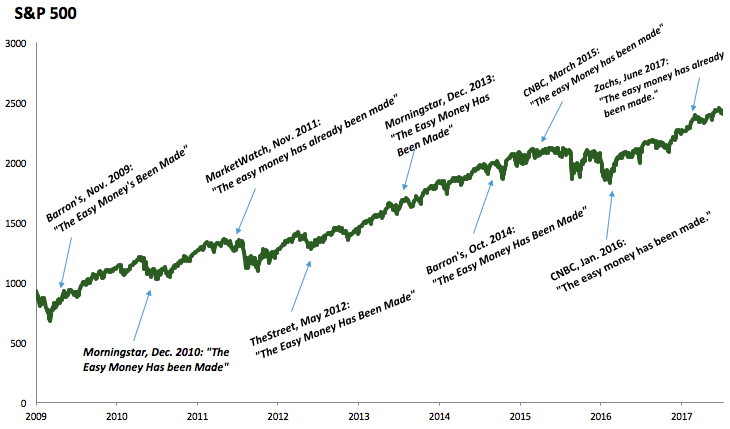

Every Great Investment Hurts

Jeff Immelt stepped down as CEO of General Electric last month. It capped 17 years of pressure by investors for moving too slow and in the wrong direction.

Immelt told the Financial Times shortly after: “Every job looks easy when you’re not the one doing it.”

No passes are given to those paid dynastic wealth to accept a challenge. But I love the quote, because it applies so well to investing.

Every great investment is born from decisions that were harder than they appear to an outsider. There are so few exceptions to this. Investors have a fascination with no-brainers, obvious decisions, and easy money. The phrases should be chapter titles in a book on the ease of deluding yourself.

A critical part of investing is distinguishing what looks easy in hindsight from what feels easy right now. They are different beasts. Opposites, even.

This is more than hindsight bias, where everything in history books seems obvious. It’s about the forward-looking risk-reward tradeoff – which is devilishly hard to quantify – actually manifesting in whether you go to bed asking yourself “What the hell am I doing?” before making an investment. Easy decisions are rarely viewed as “no-brainers” in hindsight, and vice versa.

As Immelt might say, every great investment decision looks easy when you’re not the one doing it.

Finding above-average investments requires either being smarter than others, or willing to endure more discomfort and uncertainty than others. It’s natural to focus on the former, because the industry is full of people who are either very smart or think they are. But most edges are found in the latter, specifically because the “I’m-really-smart” edges get competed into the ground. Where there’s consistent performance there’s usually intelligence. But there’s almost always a willingness to make more painful decisions than competitors.

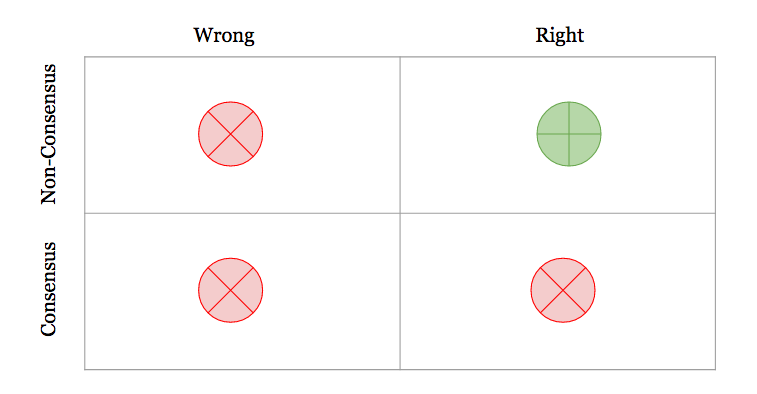

Former Benchmark partner Andy Rachleff recently told Patrick O’Shaughnessy:

Obviously you don’t make money if you’re wrong. What most people don’t realize is that you don’t make money if you’re right in consensus. Returns [or alpha] get arbitraged away. The only way you make money is by being right in non-consensus. Which is really hard.

He’s referring to Howard Marks’ 2-by-2 matrix of investment decisions, which looks like this:

Take Uber and Lyft. Such obvious ideas. But Josh Brown once joked about what it might look like if Uber pitched to Shark Tank:

Barbara Corcoran: Let me see if I understand this . You think people are going to want to get picked up by unlicensed strangers?

Yes.

Barbara Corcoran: So you’ll be competing with every transportation company in the world?

Yes. And we’ll also be having knock-down, drag-out fights with politicians and lobbying groups in almost every state and city, not to mention the fact that we’ll be responsible for the safety of millions of drivers and passengers everywhere we go.

Kevin O’Leary: What did you say your valuation would be?

We think we’ll be worth $40 billion within our first 36 months.

Or take Warren Buffett’s 2008 investments in several banks. Looks easy in hindsight – cheap! Good companies! But Buffett made his offers the same week PIMCO CEO Mohamed El-Erian told his wife to take out as much cash from the ATM as she could because the odds were so high that the banking system would collapse. You are kidding yourself if you think being greedy when others are fearful is as easy as saying it during a bull market.

Craig Shapiro recently wrote:

Spend time contemplating any new business, and you will quickly find what looks like fatal faults. The hardest part of early-stage investing isn’t finding great entrepreneurs. It’s saying “yes” to an entrepreneur despite an endless number of reasons for why the business won’t work.

The point is that risk is required for reward, but risk isn’t just quantified in spreadsheets. It’s measured by the acceptance of doubt, and a willingness to make decisions that don’t make sense to many others, specifically because the gap between your check and consensus is where outperformance lives. In the most competitive markets, it’s where any results live.

One of the Navy SEALs from the Bin Laden raid wrote a book about his life in the military. Technical skills are important to be an effective soldier, he wrote, but “one of the key lessons learned early on in a SEAL’s career was the ability to be comfortable being uncomfortable.”

Same in investing.