How I Think About Debt

Japan has 140 businesses that are at least 500 years old. A few claim to have been operating continuously for more than 1,000 years.

It’s astounding to think what these businesses have endured – dozens of wars, emperors, catastrophic earthquakes, tsunamis, depressions, on and on, endlessly. And yet they keep selling, generation after generation.

These ultra-durable businesses are called “shinise,” and studies of them show they tend to share a common characteristic: they hold tons of cash, and no debt. That’s part of how they endure centuries of constant calamities.

I love the quote from author Kent Nerburn that, “Debt defines your future, and when your future is defined, hope begins to die.”

Not only does hope begin to die, but the number of outcomes you can endure does, too.

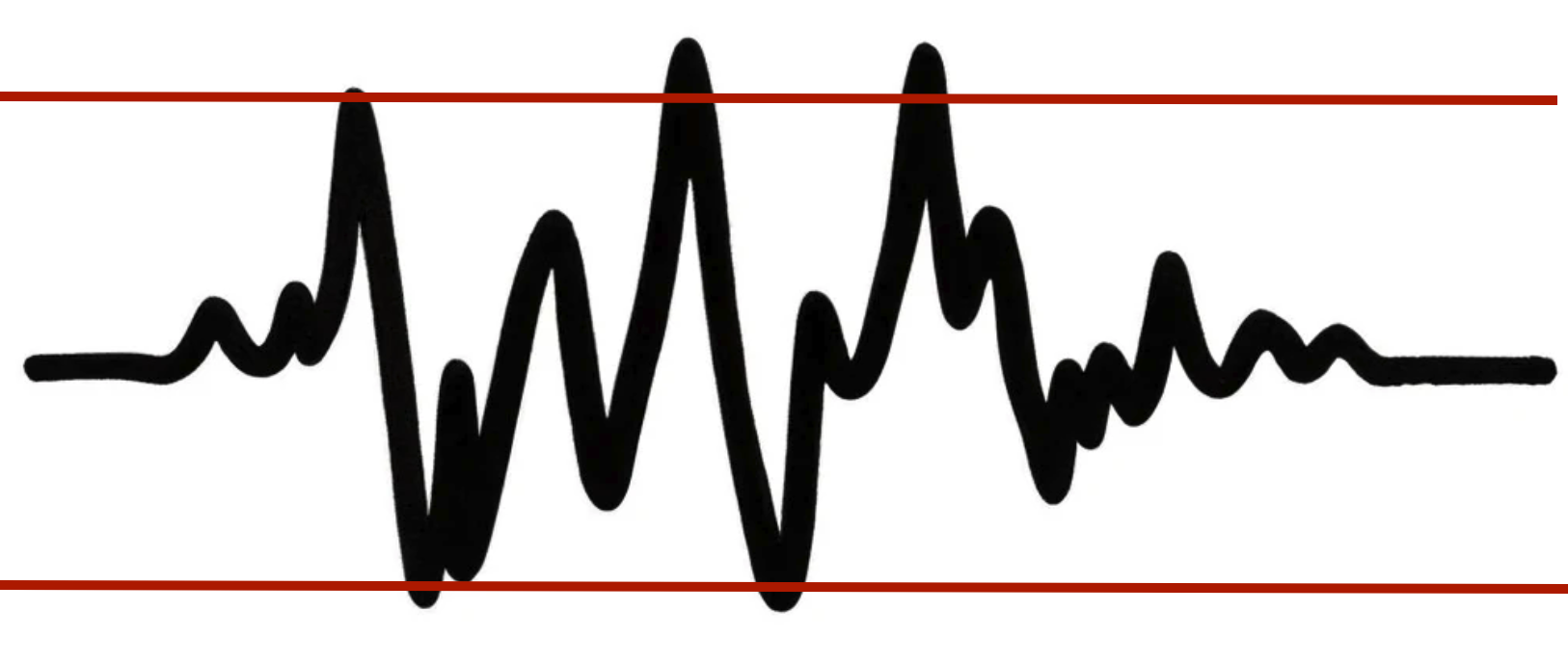

Let’s say this represents volatility over your life. Not just market volatility, but life world and life volatility: recessions, wars, divorces, illness, moves, floods, changes of heart, etc.

With no debt, the number of volatile events you can withstand throughout life might fall within a range that looks like this:

A few extreme events might do you in, but you’re pretty durable.

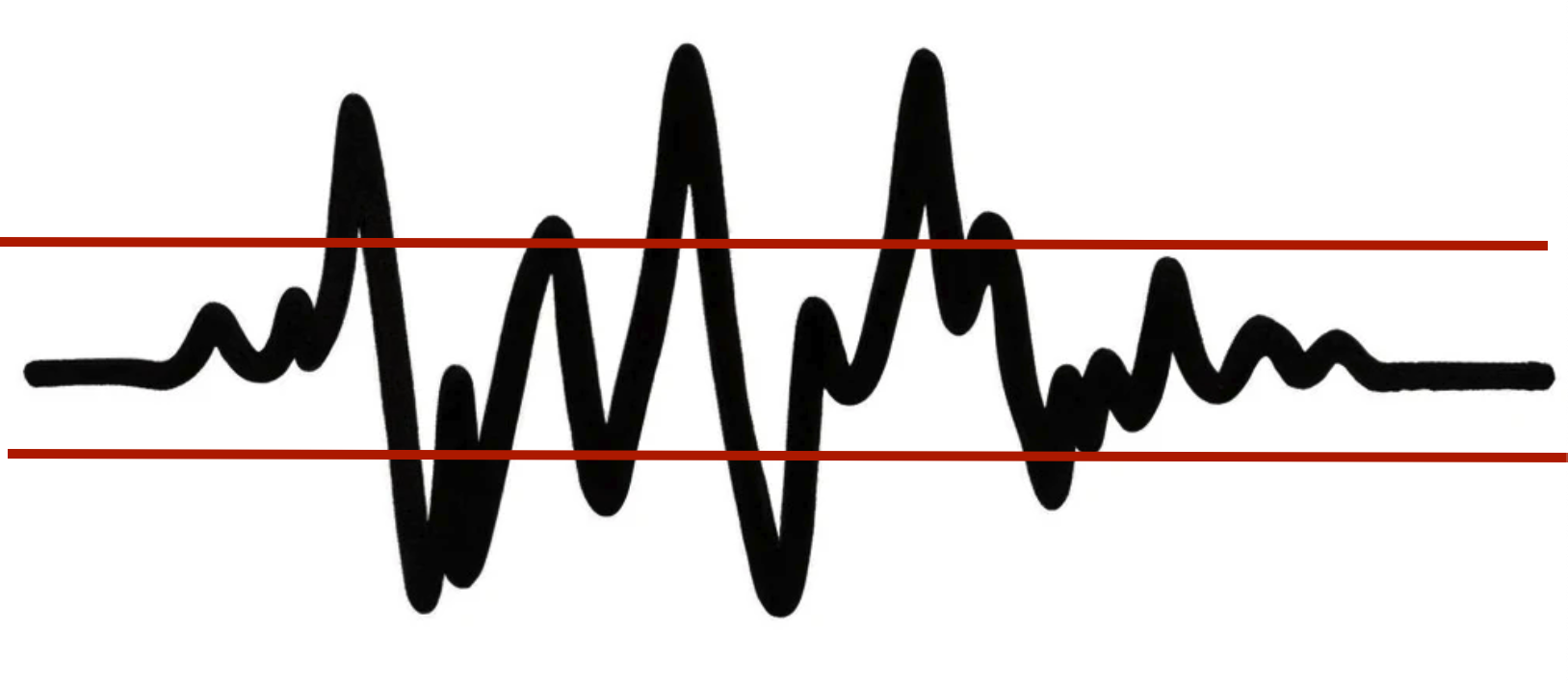

With more debt, the range of what you can endure shrinks:

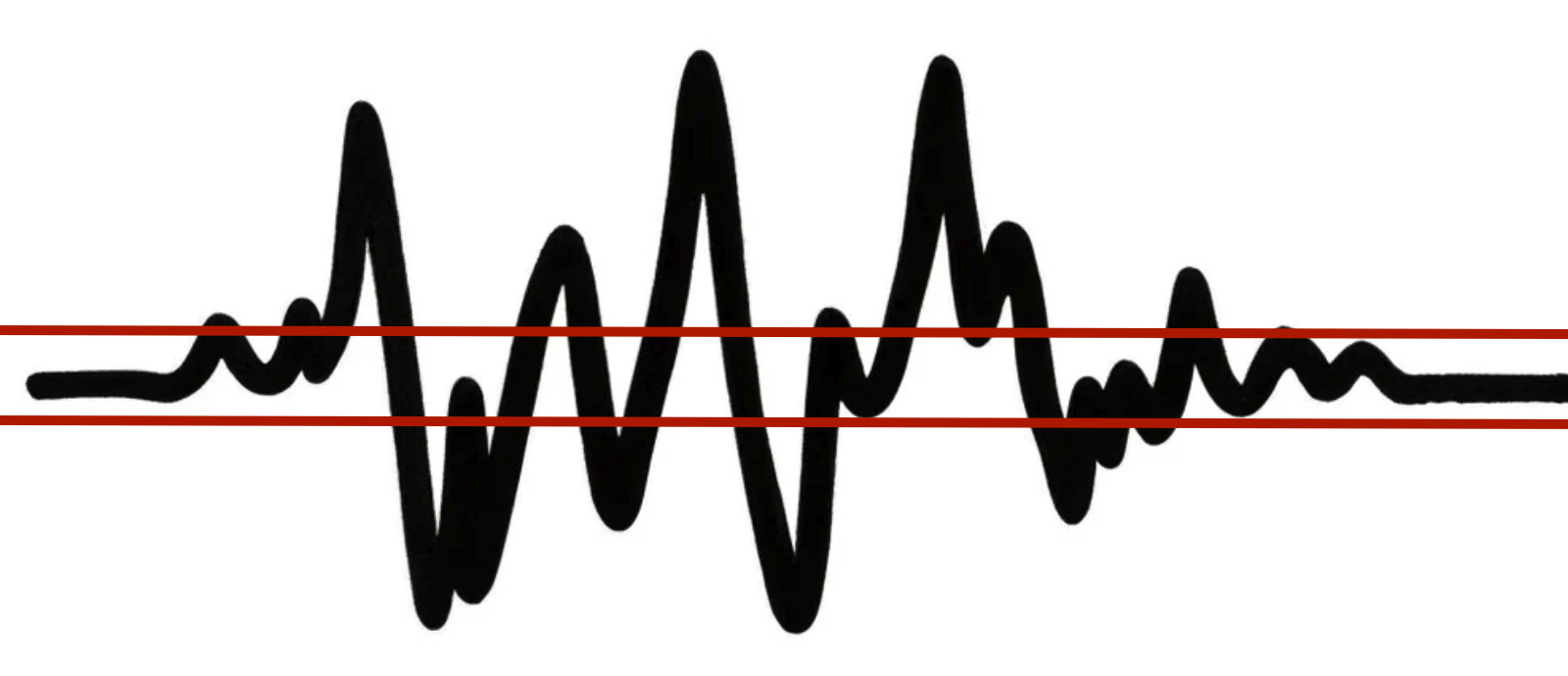

And with tons of debt, it tightens even more:

I think this is the most practical way to think about debt: As debt increases, you narrow the range of outcomes you can endure in life.

That’s so simple. But it’s different from how debt is typically viewed, which is a tool to pull forward demand and leverage assets, where the only downside is the cost of capital (the interest rate).

Two things are important when you view debt as a narrowing of endurable outcomes.

One is you start to ponder how common volatility is.

I hope to be around for another 50 years. What are the odds that during those 50 years I will experience one or more of the following: Wars, recessions, terrorist attacks, pandemics, bad political decisions, family emergencies, unforeseen health crises, career transitions, wayward children, and other mishaps?

One-hundred percent. The odds are 100%.

When you think of it like that, you take debt’s narrowing of survivable outcomes seriously.

The other is you think about the kinds of volatile events that could do you in.

Financial volatility is an obvious one – you find yourself unable to make your debt payments. But there’s also psychological volatility, where for whatever reason you can’t mentally endure your job any longer. There’s family volatility, which can be anything from divorce to caring for a relative. There’s child volatility, which could fill a book. Health volatility, political volatility, on and on. The world’s a wild place.

I’m not an anti-debt zealot. There’s a time and place, and used responsibly it’s a wonderful tool.

But once you view debt as narrowing what you can endure in a volatile world, you start to see it as a constraint on the asset that matters most: having options and flexibility.