The Difference Between a Bubble and a Cycle

Brace yourself.

According to various media sources we now have at least 14 bubbles:

- A new real estate bubble.

- A bond bubble.

- A tech bubble.

- A VC bubble.

- A startup bubble.

- A stock bubble.

- A shale oil bubble.

- A healthcare bubble.

- A dollar bubble.

- A college tuition bubble.

- A Canadian housing bubble.

- A central bank bubble.

- A social media bubble.

- A China bubble.

One economist recently gave up and just said “Everything’s a bubble.”

At a conference I attended a few years ago, Yale economist Robert Shiller said something amazing: The word “bubble” wasn’t even in the economic lexicon 25 years ago. Not in textbooks, not in papers, not in schools. But now we have bubbles everywhere.

How did that happen?

The good news is, I don’t think it did happen.

Markets have been rising and falling for centuries, but the term “bubble” is new. Since it’s new, there’s no official definition of what it is. Since there’s no definition, anyone can classify anything they want as a bubble and no one can prove them wrong. What began as a serious topic among economists has become a job-security loophole for pundits.

Shiller, in his book Irrational Exuberance, tried to solve this problem.

He says spotting a bubble is like diagnosing a mental illness. “The American Psychiatric Association’s diagnostic and statistical manual, which defines mental illness, consists of a checklist of symptoms” he once said.

He used this as a template to come up with his own checklist of bubble symptoms:

- Rapidly increasing prices.

- Popular stories that justify the bubble.

- Popular stories about how much money people are making.

- Envy and regret among those sitting out.

- Cheerleading by the media.

It’s so simple, and so smart.

But it’s far from perfect. Just as someone in a bad mood isn’t necessarily depressed, a lot of assets can give off the scent of a bubble without actually being one.

My favorite example of this is Microsoft in the early 1990s.

Shares tripled from 1988 to early 1990. People were telling stories about how computers would change the world. Bill Gates was celebrated on magazine covers as one of the youngest billionaires of all time.

Then, after years of hype, shares fell 31% in the middle of 1990.

It checked every box of being a classic bubble, down to the crushing loss of losing a third of your money in a few months.

But Microsoft wasn’t a bubble in 1990. It wasn’t anything close. Even if you start from the peak, shares increased six-fold over the next five years, and 74-fold over the next ten years. It’s only obvious in hindsight, but shares were massively undervalued at a time when they looked like a clear-cut bubble.

We see this so often.

Was Amazon a bubble in 1999? It checked all the boxes, but it wasn’t. Shares are eight times higher today than they were back then. Same with Facebook in in 2012, and GM in 1960. Was China a bubble in 2007? It looked like it, and then its economy hit a wall. But then it came roaring back just as fast. So who knows? The number of bubbles we predicted with foresight is an order of magnitude larger than the number of bubbles we now acknowledge with hindsight.

In my experience, most of what people call a bubble turns out to be something far less sinister: A regular cycle of capitalism.

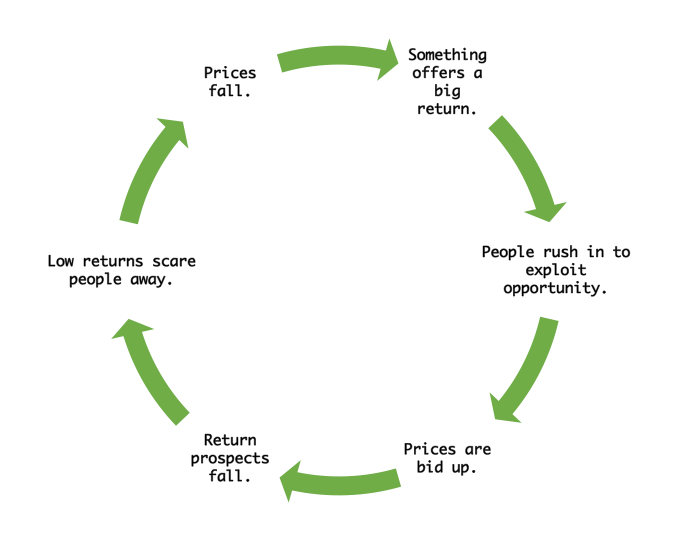

Cycles are one of the most fundamental and normal parts of how markets work. They look like this:

This cycle is self-reinforcing, because if assets didn’t get expensive they’d offer big returns, and offering big returns attracts capital, which makes them expensive. That’s why cycles are everywhere and we can never get rid of them.

To me a bubble is when this cycle breaks. I have my own definition: It’s only a bubble if return prospects don’t improve after prices fall. It’s when an asset class offers you no hope of recovery, ever. This only happens when the the entire premise of an investment goes up in smoke.

That was true of a lot of dot-com stocks, which weren’t bargains after they fell 90% because there was still no tangible company backing them up. It was true of homes in the mid-2000s, because you stood no chance of enjoying a recovery if you were foreclosed on. It was true of Holland’s 1600s tulip bubble, as the entire idea that tulips had any value went up in smoke.

But it wasn’t true of stocks in 2007. Yes, the market fell 50%. But that made it so cheap – particularly compared to the alternative of bonds – that buyers instantly came rushing back in. Prices hit a new all-time high by 2013.

It wasn’t true of the crash of 1987, when stocks fell 25% in one day, but were back at all-time highs within 18 months.

I don’t even think it was true for stocks in 1929. Yes, shares fell almost 90% by 1932. But business wasn’t broken, and valuations had never been cheaper after the crash. Adjusted for inflation and dividends, stocks were back at a new all-time high by 1936, seven years after the peak.

I wouldn’t call those bubbles. Prices went down and then came back up in a few years. What did you expect them to do? Go up 1% a month forever? Ha! It never works that way, and it never will. What we experienced were cycles, albeit huge ones.

This is an important distinction to make, because whether something is a bubble or not impacts how you invest and respond to market changes.

Bubbles should be avoided, because you risk widespread permanent loss of capital. Cycles, by and large, shouldn’t, because all they imply is that you have to be patient and humble to earn long-term returns, which is par for the course for successful investing.

If you find an asset whose price looks expensive and is probably going to fall, you likely haven’t found a bubble. You’ve found capitalism. Excesses will correct, recover, and life will go on.

But that raises a question: If we know cycles are regular, why not try to get ahead of them by buying and selling before they turn?

Because regular does not mean predictable.

We can say, in hindsight, that you should have sold stocks in 1999 and repurchased them in 2002. We can say, in hindsight, that you should have gotten out of the market in 1929 and bought back in in 1932. But not one person in a million actually achieved this, which should make us question how feasible it is do it in the future. Look at the returns of macro hedge funds, which try to ride the ups and downs of cycles and bubbles. You would not wish them upon your worst enemy.

The investing world becomes a lot less scary when you view most booms and busts as cycles rather than bubbles. Will things ebb and flow, sometimes by a lot? Well, yeah. That’s what you signed up for as an investor. But is everything with a valuation above its historic average a civilization-shattering bubble? Not by a long shot.

Three years ago Robert Shiller won the Nobel Prize in economics for his work spotting bubbles. He shared the prize with Eugene Fama, who emphatically states that bubbles can’t be spotted, and are only obvious with hindsight.

A lot of people thought this discrepancy was crazy. But it’s not.

Fama doesn’t think bubbles can be spotted. Shiller thinks they can, but they’re rare and we can never have precision on how high markets will go or exactly when they’ll turn.

What both men share is a call for humility, patience, and context. And those, more than anything, are what the history of bubbles tell us we need more of.