The Sexy Investment Premium: Opportunities in Boring Assets

For the past few years I’ve had a side gig I rarely talk about. Not because it’s a secret or because I don’t want to talk about it; but because it is, without question, unsexy.

When time and opportunity allows, I invest in government service buildings, particularly properties leased to the U.S. Postal Service.

Definitely not a subject most people want to chat about at dinner parties.

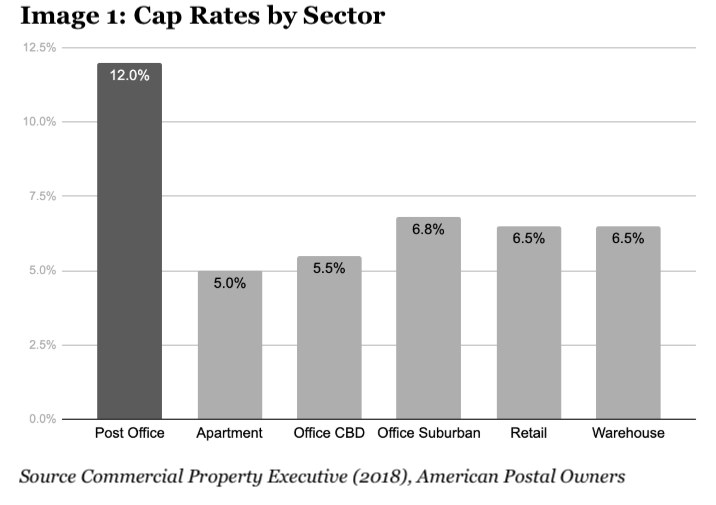

Post offices are a unique beast in the investment world. Cap rates are often 10-14% (and can be even higher). That’s on a lease where the tenant is the U.S. government. There’s virtually no risk of default and construction is first-rate since buildings must meet strict specifications.

Meanwhile, cap rates in most real estate sectors range from 3-8%, often with substantial risk.

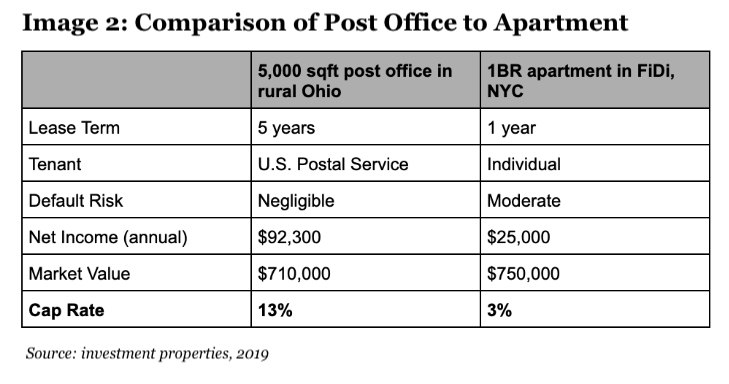

Why does a post office in rural Ohio with effectively government-guaranteed rent have a higher return than an apartment in downtown Manhattan?

Because one is substantially sexier. More investors are focused on newly constructed high-rises with skyline views, because they’re covetable pieces of real estate.

Of course, liquidity premium accounts for a substantial portion of the return differential, but I’d argue that most of the basis is psychological. Assets we want to own and talk about at dinner parties offer weaker risk/return profiles. We’re paying for hype.

This isn’t just true for real estate. It applies to startups as well.

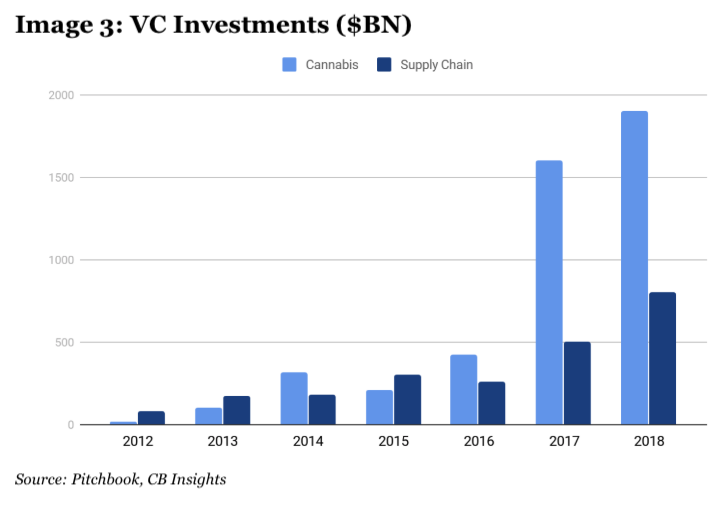

There are more venture capitalists focused on cryptocurrency, cannabis, drones, and social media than title insurance, wastewater treatment, or supply chain logistics because the former are deemed more interesting.

The result is a bidding war that leads to higher valuations and lower returns. This is true even when startups in the latter categories address larger markets with less competition (industries that are less sexy to investors are naturally also less sexy to founders) as is the case when comparing supply chain management to cannabis (see Image 3).

Elon Musk tipped his hat to this concept by using a pun to name The Boring Company. Of course, while large-scale transportation projects (particularly ones with flamethrowers as swag) are hardly “boring”, they’re not quite as sexy as electric cars or space travel. In Musk’s words, “Rockets are cool. There’s no getting around that.” So even though commuting is a more immediate pain point than colonizing Mars, SpaceX is likely to continue attracting more attention.

I’ve experienced this (on a much smaller scale) as a consumer brand investor and founder.

Consumer products is a “sexy” industry. And the more accessible (i.e., fun to talk about at dinner parties) and creative (i.e., brand and image-driven) a startup is, the more interest it garners and the more capital it raises at increasingly outlandish multiples.

That’s how we’ve ended up with approximately one million direct-to-consumer mattress and bedding companies.

But when you think about massive pain points for consumers, most of them are unsexy.

Childcare, commuting, moving, chronic pain, divorce, debt, utility services, maintenance, construction, medical bills, fraud…these are daily frustrations that disproportionately affect the happiness and wellbeing of the average American.

That’s why I’m increasingly interested in unsexy consumer investments: either goods and services in seemingly “boring” categories or more back-end, infrastructure opportunities (e.g., supply chain management and last mile delivery solutions).

In other words, categories with larger pain points and less competition. To cite another (surprisingly reasonable) quote from Musk, “You get paid in direct proportion to the difficulty of problems you solve.”

In 2020, I’m excited to do the hard work on some difficult but potentially boring topics.