You Have To Live It To Believe It

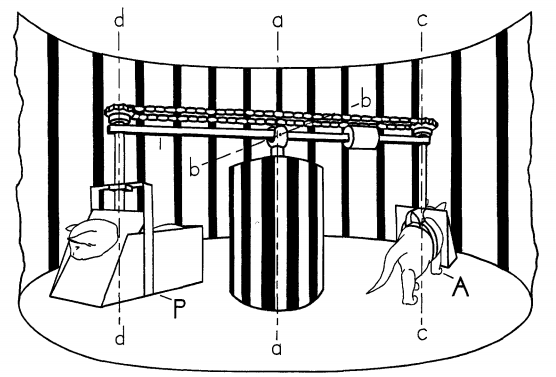

Richard Held and Alan Hein raised 20 kittens in pitch black darkness. Which is the kind of thing you should only do if it’s necessary to prove a point critical to understanding how the world works. Thankfully they did just that.

The two MIT cognitive scientists, working in the 1960s, showed that seeing the world around you was not enough to understand how it works. You had to actually experience that world to learn how to operate in it.

The scientists raised cats in total darkness to control the relationship between seeing and learning. Once a pair of kittens were old enough to walk, they were placed in a lighted box for three hours a day.

In the box was a kind of carousel, with each kitten placed in a harness. One of the cat’s legs reached the floor, and its walking movements made the carousel move in a circle. The other cat’s legs were restrained by the harness. It could see everything going on – the movement, the other cat walking around in circles – but its legs never touched the floor. It had no active control over the carousel.

After eight weeks of daily carousel walks the cats were brought into the real light-filled world to test what they had learned.

They were tested to see if they’d automatically place their paws on a surface they were about to be set down upon.

And if they’d avoid a steep ledge, walking around to a gradual ramp instead.

And whether they’d blink when an object was quickly brought close to their face.

The results were extraordinary.

100% of the cats whose legs had control over the carousel’s movements tested normal.

The cats who only watched, but never controlled, the carousel were functionally blind.

They bounded towards the steep ledge and fell straight off. They didn’t put their paws out to land on a surface. They didn’t blink when an object accelerated toward their face. It wasn’t that they couldn’t operate their bodies – they learned to do that in the dark room they were raised in. But they couldn’t associate visual objects with what their bodies were supposed to do.

The two cats grew up seeing the same thing. But one experienced the real world while the other merely saw it. The result was that one was normal; the other was effectively blind.

One of the most important topics in business and investing is whether all of us are, in some ways, like these blind cats.

Sure, we’ve read about the Great Depression. But most of us didn’t live through it. So can we actually learn lessons from it that make us better with our money?

Sure, we all know about the 2000 dot-com bust. But many – maybe most – investors and founders weren’t active back then. So do they actually understand the power of bubbles as well as those who did live through it?

My generation, the millennials, has never experienced significant inflation. We can read about gasoline lines of the 1970s and 15% mortgage rates in the 1980s. But am I as concerned about monetary policy as the Baby Boomer who does remember those things? And is the Baby Boomer as concerned as the Venezuelan who’s experienced hyperinflation?

The answer to these questions is – at best – maybe.

I say it’s one of the most important topics because it affects everyone. What I’ve experienced as an investor is different from what you’ve experienced, even if we’re from the same generation. And the generation and country you’re born into, the values instilled in you by your parents, and the serendipitous paths we all wander down are out of our control.

Investor Michael Batnick says, “some lessons have to be experienced before they can be understood.” We are all victims, in different ways, to that truth.

This report digs into the effect difference experiences we’ve had have on our ability to make smart decisions about business and investing risk.

Part 1: Blind Spots

Two events shaped the 20th century: The Great Depression and World War II.

The 1960 Democratic primary pitted a man who didn’t experience the former against a man who didn’t experience the latter. And voters took note.

John F. Kennedy grew up in one of the wealthiest American families, and the rare clan whose wealth surged during the Great Depression. His father Joe Kennedy’s life goal was to make so much money that his kids could devote their life to politics. He did just that.

In 1960 journalist Hugh Sidey attempted to gauge Senator Kennedy’s economic credentials. “What do you remember about the Depression?” Sidey asked. JFK responded candidly:

I have no first-hand knowledge of the depression. My family had one of the great fortunes of the world and it was worth more than ever then. We had bigger houses, more servants, we traveled more. About the only thing that I saw directly was when my father hired some extra gardeners just to give them a job so they could eat. I really did not learn about the depression until I read about it at Harvard.

Kennedy then leaned forward and told Sidey, “My experience was the war. I can tell you about that.” He then recounted his battle experiences for more than an hour.

Sidey later reported:

If I had to single out one element of Kennedy’s life that more than anything else influenced his later leadership it would be the horror of war, a total revulsion over the terrible toll that modern war has taken on individuals, nations and societies. It ran ever deeper than his considerable public rhetoric on the issue.

Kennedy ran against Hubert Humphrey, whose personal history was an almost mirror image of his own.

Humphrey was born in his father’s store in Wallace, South Dakota. It didn’t get much better from there. Smacked by the Great Depression, he was forced to drop out of college after a year to help his father keep the store afloat. He struggled financially for the rest of his life. It had a lasting impact on his thinking. During the campaign Humphrey said he learned more about economics from one dust storm during the Depression than he did in all his college economics courses combined (he later finished his degree).

Humphrey could relate to everyday Americans and their money problems in a way Kennedy never could -– a point he repeated often during the campaign.

But unlike Kennedy, Humphrey did not see combat during World War II. He was turned down by the Army and Navy because of colorblindness and hernias.

The Kennedy campaign turned the tables and used Humphrey’s lack of war experience as evidence that he didn’t understand something that was central to Americans’ lives. They created what was almost certainly a false narrative that Humphrey was a draft-dodger – unforgivable to American families who lost almost half a million soldiers in the war. Stumping for Kennedy, Franklin Roosevelt Jr. told crowds: “There’s another candidate in your primary. He’s a good Democrat, but I don’t know where he was in World War II.”

Both campaigns used the same logic: someone who merely read about a big event cannot fully empathize with those who experienced that big event.

Which is a point that comes up often in investing.

Two years ago Marc Andreessen said that tech stocks have been undervalued for most of the last 15 years. It partly explains why they’ve produced great returns. The cause of undervaluation, he explained, was the mental scars left by the dot-com implosion in 2000.

“If you live through one of these scarring crashes, you get psychologically marked,” he said. It scarred investors, founders, journalists, regulators, everyone. Investor Tren Griffin wrote:

I have a lot of muscle memory that resulted from the Internet bubble. There is no way you can fully convey in words the experience being in the lead car as an investor in that roller coaster. Looking at the cycle after the fact is nothing like looking ahead and not knowing what will happen next. The experience still impacts the way I think and act.

That last point is important, because something began changing in Silicon Valley over the last few years. Andreessen again:

One thing that’s happening is now enough time has passed that enough kids are coming to the Valley who don’t have a memory of the crash. They were like in 4th Grade when it happened. We get in these weird conversations where we’re telling them cautionary tales of what happened in 1998, and they look at you like you’re a Grandpa.

We have a new generation of people in the Valley who say, ‘Let’s just go build things. Let’s not be held back by superstition.’

This new generation might help explain why Silicon Valley risk-taking grew over the last five years. The number of VC funds, the number of VC-backed deals, the valuations those deals fetch, and the number of college grads to get into startups has surged. The typical Silicon Valley founder in your head might look like a 21-year tinkering in their dorm room, and some are. But the median age of a startup founder is actually 40. Yet even a 40-year-old was likely in college during the dot-com rise and fall. They avoided the carnage. So they think about risk and reward in totally different ways than a 40-year-old founder did five or 10 years ago.

This is not just anecdotal.

In 2006 economists Ulrike Malmendier and Stefan Nagel from the National Bureau of Economic research dug through 50 years of the Survey of Consumer Finances – a detailed look at what Americans do with their money.

In theory people should make investment decisions based on their goals and the characteristics of the investment options available to them at the time (things like valuation and expected return). But that’s not what people do. The research showed that people’s lifetime investment decisions are heavily anchored to the experiences those investors had with different investments in their own generation – especially experiences early in their adult life.

They wrote:

Our results explain, for example, the relatively low rates of stock market participation among young households in the early 1980s (following the disappointing stock market returns in the 1970s depression) and the relatively high participation rates of young investors in the late 1990s (following the boom years in the 1990s).

This holds true across asset classes. Ten-year Treasury bonds lost almost half their value from 1973 to 1981, adjusted for inflation. Those who lived through these blows invested considerably less of their assets in fixed-income products than those who avoided them due to the luck of their birth year.

Back to my generation, the Millennials, who have never experienced inflation: When we invest on our own, we put 59% of our assets in cash and bonds, and 28% in stocks, according to UBS Wealth Management. And of course we do: Many of us started making money in the teeth of the Great Recession and the largest bear market in generations, which also happened to be the period when bonds not only preserved but grew wealth as interest rates fell to 0%. That’s our history. That’s what we know. And what we know is more persuasive than what we read.

The Financial Times interviewed Bill Gross, the famed bond manager, last month. “Gross admits that he would probably not be where he is today if he had been born a decade earlier or later,” the paper wrote. His career coincided almost perfectly with a generational collapse in interest rates that gave bond prices a tailwind. That kind of thing doesn’t just affect the opportunities you come across; it affects what you think about those opportunities when they’re presented in front of you. This was Andreessen’s point: In hindsight we know tech stocks were undervalued for most of the 2002-2015 period. But the generation that lost most of their money in the tech bust didn’t even recognize that opportunity. It took a new generation who lacked the scars of the bust to see it.

Our own unique experiences impacts more than just investing behavior.

In a study of men graduating from college between 1979 and 1989, Yale economist Lisa Kahn found that those entering the labor market during poor economic times earned 7% less than those graduating in a strong economy. That gap lasted seemingly indefinitely: 17 years after graduation, Kahn found those who began their careers in recession still earned less than those who began when the economy was strong. You can imagine that a group who experiences that kind of pain will have different views about economic policies than a group who happened to graduate during a booming economy.

And it’s not because one group is smarter than another; most of it is just the chance of what generation they were born into. Where you were born matters too. European economies have tended to be more risk-averse, downside-protection, savings-net-oriented than the U.S. economy. Why? Perhaps in part because European economies spent most of the 20th Century either collapsing or rebuilding from two world wars, both of which completely wiped out the life savings of tens of millions of residents. America paid a human price in combat, but the wars were an economic boon. Compare that to Germany and Japan in the years following 1945, when a full-blown humanitarian crisis developed. At the end of the war German farms only produced enough food to provide its citizens with 1,000 calories a day. Part of Japan’s current demographic decline is due to a cultural preference for small families, which started when the government created policies and incentives to reduce births as the country teetered on famine in the late 1940s. You can’t expect countries whose experiences are that divergent from our own to have similar views about economic and social policies.

And this goes beyond economics.

There are theories that big wars tend to happen 20-40 years apart because that’s the amount of time it takes to cycle through a new generation of voters, politicians, and generals who aren’t scarred by the last war. Other political trends – social rights, economic theories, budget priorities – follow a similar path. Whether you agree with her or not, Alexandria Ocasio-Cortez’s response to Joe Lieberman’s jab that she’s not the future of the party – “New party, who dis?” – echoes a trend that’s been followed for centuries. JFK’s inaugural address declared:

The torch has been passed to a new generation of Americans – born in this century, tempered by war, disciplined by a hard and bitter peace, proud of our ancient heritage – and unwilling to witness or permit the slow undoing of those human rights to which this nation has always been committed.

The Civil Rights Act – started by Kennedy, finished by Johnson – is an example of something that would have been impossible in one generation but was doable in another generation who grew up with different experiences and views than their parents.

Part 2: Can We Ever Learn?

The big question is: Which investing group is better off? The veterans who lived through a crash and came out paranoid, or the newbies who never experienced it and are now willing to take bigger risks?

I don’t think there’s ever a clear answer to that question.

Long-term business and investing skill is the intersection of getting rich and staying rich. Different generations whose formative experience was calm and growth-oriented may be better at getting rich – they’re willing to take risks. But generations whose upbringing was punctuated by crash and decline may be more attuned to staying rich – conservatism, room for error, and rational pessimism. The best investors find a balance between the two, toggling between the two traits at the right time. But that’s rare. And the reason it’s rare even among smart people is because the psychological scars of our experiences don’t discriminate on IQ. Or more specifically, they sit above IQ in the information hierarchy that people use to make decisions.

Michael Batnick has made the point that having experienced a big event doesn’t necessarily make you better prepared for the next big event. Few bond investors – even grizzled veterans – have lived through a sustained rise in interest rates. But, he writes:

So what? Will the current rate hike look like the last one, or the one before that? Will different asset classes behave similarly, the same, or the exact opposite?

On the one hand, people that have been investing through the events of 1987, 2000 and 2008 have experienced a lot of different markets. On the other hand, isn’t it possible that this experience can lead to overconfidence? Failing to admit you’re wrong? Anchoring to previous outcomes?

It’s never clear one way or another. People with different experience than us aren’t necessarily smarter. They just see the investing world through a different lens.

Part of why learning through experience isn’t necessarily good or bad is due to the lessons we take away from experience.

Jason Zweig of The Wall Street Journal once noted:

I often like to say that people are too good at learning lessons, and the lesson that people should have learned after the Internet bubble burst in early 2000 was that day trading is a really bad idea. But people are too good at learning lessons, so they learned an overprecise lesson, which was that day trading Internet stocks is a really bad idea. So in recent years we see the same people who day-traded internet stocks going into day-trading foreign currency.

I have a theory about why this hyper-specific learning happens.

My son is three. He’s amazing. But he’s three. So he doesn’t know very much.

What’s amazing about a three-year-old is that they learn fast, but virtually everything they know came from what they’ve observed and experienced firsthand. He’s never sat through a history lecture, spent an afternoon analyzing stock charts, or had a long dinner with someone from another country. Everything in his head came directly from an experience he’s had. He therefore has no idea how most things work. Imagine trying to get him to understand the nuances of NATO; impossible. Or LIBOR; can’t do it. Enormous, important chunks of the world do not exist in his brain. He has no concept of them.

But he doesn’t walk around confused all day. He understands his world perfectly. It’s a world shaped by, and explained with, the few mental models he’s picked up in his three years. Ice cream is good. Blankets are warm. Toys are fun. Naps are not. I don’t need a bath. That’s his world. And everything he comes across fits into one of those simple three-year-old mental models that he’s built in his head.

When his parents tell him it’s time to put his toys away, or that he can’t eat ice cream for breakfast, his frustration is caused by experiencing something that doesn’t fit into his mental models. Ice cream is good, so if mom says I can’t have it, that’s not good and I’m going to cry. He has no concept of a balanced diet, or the consequences of a poor diet, even if we explain it to him. But, in the moment, he’s not looking for an explanation. He’s trying to match the world he lives in to a mental model he has in his head. Even though he knows almost nothing, he doesn’t realize it, because he tells himself a coherent story about what’s going on based on the little he does know.

And we all do this, regardless of age.

I don’t know what I don’t know. No one does. But we can’t walk around confused all day. Nassim Taleb says “I want to live happily in a world I don’t understand.” Which is exactly what we do. We take the world we live in and try to make a coherent story out of it based on the mental models we’ve developed during our lifetimes.

Those models are only useful when they’re simple. That’s when they become automatic. Complex, nuanced models – like the art of negotiating – are hard. But simple ones like “say thank you when someone helps you” – are easy to grasp.

This is where Jason’s point comes back in. Specific lessons are easier to build mental models with, so they’re what we take away from experience. Learning that you’re susceptible to the siren song of bubbles is hard and nuanced. But learning that “tech stocks hurt me so I should avoid tech stocks in the future” is an easy lesson. My son could pick it up. It doesn’t matter that it’s not a very good lesson. It’s an easy one, so we use it.

There’s a related issue here about how we process the memories of our experiences.

In his book on World War II, historian Joseph Balkoski writes that “One firm lesson that serious World War II researchers have learned is that the reliability of human memory varies drastically from one veteran to the next.” Veterans recalled experiences that were verifiably false. Time, Balkoski writes, “can play subtle tricks on the mind, and the historian’s thorniest problem is to separate those rare fully substantiated accounts from the more typical yarns that time has established.”

Daniel Kahneman calls this the “experiencing self” and the “remembering self.” They can be two completely different minds.

Memories of big events are influenced by a few punctuated moments, not the full story. Kahneman once gave the example of a study showing how people remember colonoscopies:

[What influenced memories was] determined completely differently from what we would have thought. It was simply an average of the worst moment in the colonoscopy, and how badly it hurt when the procedure ended.

Those two variables really gave you excellent prediction of, when you ask people, “Would you want to have another one of those, or would you rather have another painful procedure?” Or you ask them, how much total pain was it? How bad was the whole experience?

He later wrote:

The experiencing self is the one that answers the question: “Does it hurt now?” The remembering self is the one that answers the question: “How was it, on the whole?” Memories are all we get to keep from our experience of living, and the only perspective that we can adopt as we think about our lives is therefore that of the remembering self.

An investing version of this came a few years ago. The S&P 500 gained 27% in 2009 – a fantastic return. Yet when asked in early 2010, 66% of investors thought it fell that year, according to a survey by Franklin Templeton. The market then rose 31% in 2013. That was the fifth-best annual return since World War II. But a 2014 Gallup poll asked 1,000 active investors how much they thought it increased, and only 7% knew the gain was over 30%. One-third thought it was flat or declined.

Perhaps the explanation for this gap between experience and memory is the market trauma that took place in early 2009, or the political circus of 2013, scared investors enough to create specific memories that were stronger and easier to recall than the actual overall experience. It’s also an example of relying on mental models that are simple and easy to recall, even if they’re not complete.

The imperfect side of memory complicates the question of “can we learn lessons without experiencing events?” It’s not even clear that people who experience big events can learn from their own past. They can be influenced by their past in a way that guides their future decisions. Learning is something different.

But let’s assume you go out of your way to be as open-minded as possible, becoming a student of history and putting yourself in others’ shoes. Can you learn?

Yes, of course. But there are endless asterisks.

The hardest part of studying history is that you know how the story ends, often before you begin researching a topic. And I don’t think you can un-remember that fact when reading about an event. Particularly difficult is attempting to put yourself in someone’s shoes and imagining their emotions when you know how the story ends but they, at the time, did not.

SEAL Team 6 gained fame after it killed Osama Bin Laden. Video games and movies were made glorifying the raid. But President Obama later said the odds placed on whether Bin Laden was actually in the target house were 50/50. Last year I heard one of the SEALS involved in the mission speak at a conference. He said, regardless of whether Bin Laden was in the house, the team felt the odds they’d all be killed in the mission were also 50/50. So here we have a 75% chance that the raid would have ended in disappointment or catastrophe. Which is not something the people creating glorified video games of an epic adventure think about. They highlight the badass success and glory, because that’s how the story ended. But no one knew that before or during the raid.

A corollary in business and investing is that there is a thin line between bold and reckless. The hindsight view of outcomes can blind us to other scenarios that easily could have happened, which makes learning lessons about how much risk we should take in the future difficult.

I can say “2009 taught us that you should buy when there’s blood in the streets.” But it’s easy to forget how bad the financial crisis was, and how different the outcome could have been. Fed chairman Ben Bernanke allegedly told a group of congressmen in 2008 to prepare for martial law within 48 hours if the banking system were allowed to collapse. That’s the kind of thing that’s easy to forget as we look back and learn lessons.

Same with business. We think Mark Zuckerberg is a genius for turning down an offer to sell Facebook to Yahoo. But people criticize Yahoo with as much passion for turning down its own buyout offer from Microsoft. Hindsight is the only difference between the two. What is the lesson for entrepreneurs here? I have no idea. I don’t think anyone does. That’s the point.

“The customer is always right” and “customers don’t know what they want” are both accepted business wisdom. Examples of both are only known with hindsight, and it’s impossible to think about these topics with an open mind when you know the eventual outcome of how certain products perform.

Another hard part about learning vicariously is that there’s a difference between learning and learning so well that it compels you into action.

A 13-year-old girl being killed by a drunk driver is something everyone reading this article will agree is atrocious. Yet virtually all of us will say it’s atrocious without taking further action. But Candace Lightner’s daughter was that 13-year-old girl, so she created Mothers Against Drunk Driving to do something about it. Personal experience is often what pushes you from “I get it” to “I get it so well that I’m going to do something about it.”

Same in investing. Spreadsheets can model the historic frequency of big declines. But they can’t model the feeling of coming home, looking at your kids, and wondering if you’ve made a mistake that will impact their lives. Studying history makes you feel like you understand something. But until you’ve lived through it and personally felt its consequences, you may not understand it enough to change your behavior.

Anchoring to your own history is not a problem with a clear and simple answer.

There is no, “Just do X and you can overcome this problem.”

It’s one of those things where the best we can do it to become a little more aware of its presence.

Going out of your way to speak with people whose backgrounds are different than yours, knowing that their view of the world may look nothing like your own, though they are just as sure of their views as you are of yours, is a humbling thing. But it’s so important to expand your mind to the range of possibilities you may come across as an investor. I think it’s probably the most important kind of learning an investor can accomplish – going out of their way to figure out what kind of worldview and experience they haven’t had that others who have just as much influence over market outcomes have had. As Jim Grant says, “Successful investing is getting others to agree with you … later.” If those other people will never agree with me because their personal history blinds them to my view, then my view and my forecasts may never become reality. A practical side of this is having room for error in your decisions and forecasts, knowing that your view of the world is a tiny fraction of all the other views that can influence the economy.

Another takeaway is remembering that people whose views and decisions look crazy to you may be less crazy than you think, because they’re being made by people whose views on risk and reward were shaped in a different world than you’ve experienced. I don’t understand why someone would want to put all their money into gold after the financial crisis, or crypto in recent years. But my financial experience is probably different than people who have done those things. I don’t get why anyone would want to become a lawyer, or a zoologist, or a pilot; those things don’t appeal to me at all. But maybe all lawyers and zoologists and pilots experienced something in their life that made those jobs appealing. And maybe they’d be appealing to me if I had those same experiences. When you realize that other people can make decisions that look crazy to you but make perfect sense to them because they’ve experienced something you haven’t, you become less cynical about the investing industry and more focused on whatever works for you. We should always try to make people better informed, but with the idea that people with the same information will often come to different conclusions.

“Personal finance is more personal than it is finance,” says Carl Richards. To each their own. I always try to remember that before criticizing others’ decisions. “Your yesterday was not my yesterday, and your today is not even my today,” writes the book Our Kids.

When the study was over the blind cats were left in a fully lit room. Forty-eight hours later, all were effectively normal, regaining their “vision” and learning how to match the world around them to their movements.

Eight weeks of seeing their world taught them virtually nothing. Two days of experiencing it, and they had it all figured out.