Breaking Points

Guest post by Ted Lamade, Managing Director at The Carnegie Institution for Science

Two weeks ago, Mitt Romney wrote an opinion piece in The Atlantic titled, “America Is in Denial”. The piece highlights numerous potentially “cataclysmic events” facing the nation, namely droughts out west, inflation, rising debt levels, profligate government spending, melting ice caps, illegal immigration, and the events of January 6th. Interestingly though, Romney argues that the most significant threat is actually not the events themselves, but rather Americans’ refusal to address them.

The question is why?

Romney believes it is due to our “powerful impulse to believe what we hope to be the case — We don’t need to cut back on watering, because the drought is just part of a cycle that will reverse. With economic growth, the debt will take care of itself. January 6th was a false-flag operation.”

You may or may not agree with Romney’s causes for concern, but for the moment let’s assume that at least a few have merit. If so, why do people so rarely act before a crisis occurs? Why do we instead choose to bury our heads in the sand and hope for the best?

The answer is actually quite simple — no one knows when something will break. It could be imminent or many years away. No. One. Knows. As a result, people tend to push the throttle until it does.

History is full of examples. It’s why governments don’t reform until it’s too late, real estate developers believe there is always room for one more building….theirs, the Federal Reserve is almost always late to “pull the punchbowl away” during an economic expansion, and why so many investors rarely de-risk in the later stages of a bull market.

The trouble is that when things do eventually break, they tend to break more suddenly and quickly than anyone had imagined. It happened to the Soviet Union with the fall of the Berlin Wall in the late 1980’s, real estate developers in the early 1990’s, dot.com companies in the late 1990’s, banks and homeowners in the late 2000’s, energy companies in the mid 2010’s, and many investors over the past year, especially those focused on high growth tech, crypto, and ESG.

During these moments, confidence and clarity evaporates and is replaced by pessimism and doubt. People once viewed as oracles and geniuses morph into scapegoats and know-nothings. Endless opportunities filled with sky high potential become toxic. Hope turns to despair.

Ironically though, as hard as it is to believe in the moment, these are precisely the times that provide the fertile topsoil for future portfolio returns. The trouble is, something has happened over the past two decades that has made it more difficult to plant seeds.

Fifteen to twenty years ago, the vast majority of portfolios were largely invested in public stocks and bonds. A lot has changed since then, mainly because investors have increased their allocations to private markets, materially in some cases. In fact, the Economist reported last week that the amount of money invested in or committed to private equity has “swelled from $1.3 trillion in 2009 to $4.6 trillion today” and that many allocators have more than doubled their allocations to private equity during this time. As an example, Brown University’s endowment had less than 20% in private equity in 2009. By 2021 it stood at nearly 40%. In some cases, the increase is even more pronounced. Look no further than The University of Pennsylvania. In 2002 its endowment had 2.3% allocated to private equity. By 2009 it had roughly tripled its allocation, but was still relatively modest at 6.3%. However, by 2021 it had increased its allocation to private equity by nearly six times to 36%!

For many investors (Brown and UPenn included), this has led to stronger performance and lower volatility (or at least the illusion of lower volatility). However, as with most things in life, this decision has its tradeoffs. In this case, given that these portfolios are less liquid today, the ability to rotate capital and be opportunistic has diminished materially.

How so?

Just look at how differently private and public markets react during these breaking points.

Private markets seize up. Anchored to valuations floated in more ebullient times, sellers go on “strike”. Banks that were once willing to lend at any rate get “alligator arms’’ and offer punitive rates, if they are even willing to lend at all. Meanwhile, private equity firms dedicate more attention to existing portfolio companies and less to sourcing, while limited partners request (or at least hope) that capital calls slow down. This leads to a situation where, as Tomasz Tunguz wrote in a recent post, the difference between where buyers and sellers will transact becomes “less of a spread and more of an abyss.” As a result, “the market seizes up, like a combustion engine without oil. No one trades. Investors pack their vests into a rolly-suitcase and head to the beach.”

Meanwhile, the public markets respond much differently. Sellers cannot strike because securities are traded daily, bank financing is not needed to deploy capital, less attention is required for existing investments, and capital calls are practically non-existent. The result is that while the ride for public market investors is much more uncomfortable, the opportunity to plant the seeds for future returns is significantly greater. Today is no different with most indexes down 20%+, some sectors down more than 30%, and one out of every five stocks in the Russell 3000 down more than 80% from their all-time highs.

The result, however, is that those with heavy allocations to private equity today are a bit paralyzed. While they shouldn’t expect a lot of capital calls from their managers, they still have to make sure they have enough in reserve to fulfill them if they do. Meanwhile, since private equity firms are slower to recognize losses, its percentage in many portfolios has only increased as a result of public market losses, which makes it even more difficult for allocators to rotate capital into beaten up parts of the liquid portfolio.

So where does that leave us?

Private markets have been very good to investors for the past two decades. Whether this success will continue warrants a lengthier discussion, but even if it does, this decrease in portfolio liquidity and flexibility is inevitable. In some cases, this is likely perfectly fine, in particular for those who place a high value on reducing volatility (or, once again, the perception of lower volatility). However, for those willing to embrace volatility and the mark-to-market nature of the public markets, these breaking points are the moments you should live for.

The fact is, markets and managers don’t sell off 20-30% very frequently. Individual stocks sell off more than 50% even less often. This means that potential future returns for many stocks and actively managed funds are meaningfully higher today than they were just a few months ago.

Given this backdrop, what should one do during breaking points like the one we are currently enduring?

Ben Carlson makes a pretty compelling case in a recent post for simply beginning to add to index funds. The rationale? While stocks (and managers) can go out of business, index funds cannot. It’s hard to argue with that. Simply adding to your market exposure during these moments is the safest and most straightforward way to take advantage during these moments. However, given how much more certain parts of the market have sold off, an investor can accentuate those index returns by adding to individual stocks or managers.

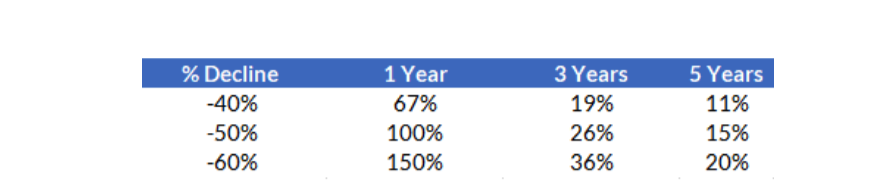

The math is simple. If a stock or a manager is down 40% and reclaims its prior high within one year, it will generate a 67% return. While this is unlikely, 2020 showed that it is not impossible. A more reasonable possibility though is that it will take three years. If so, this would equate to a 19% annual return. How about five years? 11%. Nothing extraordinary, but a relatively conservative assumption.

The scenarios only improve from there:

The question is, how do you identify the right companies or managers? Those that will “right the ship” and reclaim their prior highs? The ones that will not close up shop at the bottom, go bankrupt, or suffer from permanent impairment like many may in the wake of this break?

Strong Leadership: This is where it all starts. Trustworthy leaders who have been through tough times before, are materially invested, and are committed to getting the business through to the other side are invaluable during these moments. To get our country out of the current mess we find ourselves in, Mitt Romney believes the country needs to identify the next generation of great leaders…leaders like Churchill, Lincoln, Reagan, Walesa, King, and Zelensky. The same can be said for investors.

Aligned Incentives: You can have the best people in place, but if they aren’t properly incentivized, don’t be surprised if their actions diss appoint you. I wish this weren’t the case, but it’s simply human nature. If employees are sitting on a bunch of underwater equity options, there will be a talent exodus. If a fund is well below its high water mark, employees often will leave. It’s simply not worth it for them to stay. They have lives to live, families to care for, and opportunity costs to consider. It’s hard to do, but companies and/or funds that attempt to fix this alignment issue give themselves a better chance to retain talent and get to the other side.

Durability: For companies, this equates to having a strong balance sheet and being profitable (or at least a path to profitability). It means having enough cash on hand to not need to turn to others for more. For funds it means having a loyal set of partners, those who aren’t going to panic and pull their capital at precisely the worst moments. It also means having a fair fee structure that makes investors feel like they’re not getting ripped off across the cycle and a cost structure that enables them to withstand a significant drawdown.

Ability to “Flip the Switch”: Breaking points typically put a number of companies and funds out of business. For those that do make it through though, that’s just half the battle. In order to succeed on the other side, they need to be able to “flip the switch from defense to offense”. If they can, they can chart a course for a decade or more of strong returns.

Reasonable Valuations: You may have the prior four in place, but if a stock or fund is still overvalued after a selloff, continued multiple compression can wipe out any (and all) fundamental value creation. Valuations don’t need to be extremely cheap, but they should at least be reasonable.

These aren’t the only qualities to look for, but they’re good ones to start with. If a company or fund possesses them, you’re likely to be rewarded for deploying capital into them during breaking points.

In terms of when to deploy capital, I really can’t say it any better than Warren Buffett did in quote that Akre Capital highlighted in their recent second quarter letter in response to a question about whether this tough first half to the year is a prelude to more losses or the bottom.

“What is likely is that the market will move higher, perhaps substantially so well before either sentiment or the economy turns up. So, if you wait for the robins, spring will be over.”

Said another way, it’s impossible to know when the perfect time is to start investing into a downturn, so now is as good a time as ever to start planting those first seeds.

Otherwise just commit to privates and avoid the issue altogether.