Write Two Letters

Guest post by Ted Lamade, Managing Director at The Carnegie Institution for Science

William Halsted is widely regarded as one of the “Fathers of Modern Surgery.” He is also known for being an extremely confident surgeon, co-founding Johns Hopkins Hospital, creating multiple surgical techniques, introducing sterilization procedures in the operating room, helping develop anesthesia, and creating the first formal surgical residency training program in the United States.

One of the notable surgical techniques Halsted pioneered was the “radical mastectomy”, which was a novel approach to treating breast cancer. Designed to go well beyond the breast tissue, the procedure would remove pectoral muscles, the mammary gland, lymph nodes under the armpit, and even extend down to the ribcage if necessary in an attempt to more effectively rid the patient of malignant cells. The radical mastectomy quickly became the preferred method for treating breast cancer and would remain so for decades. There was just one problem. It didn’t work. Halsted was wrong.

Instead of curing breast cancer, the radical mastectomy was overly invasive, debilitating, and ineffective for most patients. Yet, Halsted failed to acknowledge this reality. In fact, he and countless other surgeons continued to perform it even as studies increasingly showed that the ultimate survival from breast cancer had more to do with how extensively the cancer had spread before surgery than how extensively a surgeon operated.

The logical question then is, why did Halsted continue performing and promoting the radical mastectomy in the face of disconfirming evidence?

As Siddhartha Mukherjee describes in his seminal book on Cancer, “The Emperor of all Maladies,”

The Gospel of the surgical profession was ideally arranged to resist change and to perpetuate an orthodoxy. Rather than address the real question raised by the data – did radical mastectomy truly extend lives? – they clutched to their theories even more adamantly. Where others might have seen reason for caution, Halsted only saw opportunity.

Halsted was blinded by what he wanted to believe. Instead of seeking the truth, he sought confirming evidence. When the results weren’t what he had hoped for, he would often make the case that he simply needed to go further.

Halsted would eventually stop performing the procedure, but instead of denouncing it publicly, he chose to turn his attention to surgical innovations on other parts of the body. This led to a subsequent and longer-lasting problem. While Halsted physically retreated from the radical mastectomy, his failure to accept responsibility and publicly denounce it was part of the reason why surgeons continued to perform the radical mastectomy for decades.

It wasn’t until a surgeon named Bernard Fisher entered the picture nearly fifty years later to fully end the radical mastectomy. Despite sustained pushback from the medical community, Fisher repeatedly made the case that early-stage breast cancer could be more effectively treated through a combination of localized surgery, radiation therapy, chemotherapy, and/or hormonal therapy. His approach was finally recognized in the 1985 when he was awarded the “Albert Lasker Award for Clinical Medical Research” for his pioneering studies that led to a dramatic improvement in survival and in the quality of life for women with breast cancer.

Why did this happen? Why did Halsted double down on his faith in the radical mastectomy instead of acknowledging its flaws? Why didn’t he denounce it after he stopped performing it? The answer is that Halsted had crossed the thin line from confidence to overconfidence and couldn’t go back.

Confidence

Confidence is something I think about a lot because it pervades nearly every walk of life. Every successful person I know has a lot of it. Yet, so does every person who has pushed the envelope too far, taken too much risk, and eventually run their company, organization, fund, team, or even life into the ground.

So, what differentiates someone with a healthy amount of confidence from someone with too much of it? In my experience, people with the right amount of confidence share the credit when they succeed, but more importantly, accept the responsibility when they fail. This combination translates into an ability to admit when they’re wrong and change direction if needed.

William Halsted was a brilliant man who achieved numerous meaningful things in his life. Yet, his overconfidence placed a stain on an otherwise tremendous career simply because he couldn’t acknowledge his error and accept responsibility for it.

Halsted is far from alone. Overconfidence is everywhere in life. In finance, it is what caused John Merriweather, Dick Fuld, and Jeff Immelt to destroy billions in shareholder value. In sports, Barry Bonds, Roger Clemens, and Pete Rose are three of the greatest baseball players of all-time, yet none are in the Hall of Fame because of it. In entertainment, Martha Stewart, Michael Eisner in his last few years at Disney, and John Antico at Blockbuster all fell victim to it. In politics, the list is simply too long to get started.

Given this backdrop, how do you know when you have found someone with the right amount of confidence? Let’s start by taking a look at someone who took a very different approach.

Imagine This

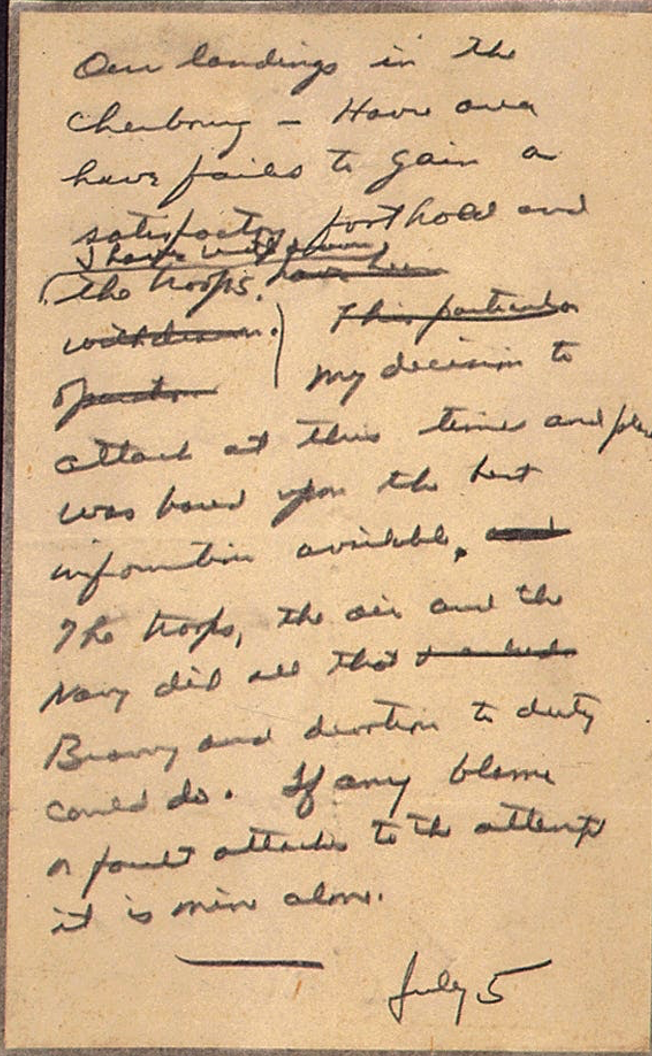

Imagine this scenario. At a critical moment in a battle, a general makes a decision that will likely determine the fate of countless troops, the war, and maybe even the world. Knowing the decision’s significance, the general writes this letter to his superiors. It reads,

“Our landings have failed to gain a satisfactory foothold and I have withdrawn the troops. My decision to attack at this time and place was based upon the best information available. The troops, the air, and the Navy did all that bravery and devotion to duty could do. If any blame or fault attaches to the attempt, it is mine alone.”

Now, what if I told you this is an actual letter from World War II, but wasn’t released until years after the war had ended? What would you think if I told you the events described in the letter never actually occurred?

Confused? You should be. We don’t see things like this happen very often anymore.

On the eve of D-Day in 1944, General Dwight D. Eisenhower wrote two letters. In the first, Eisenhower wanted to praise the Allied soldiers’ for successfully gaining a foothold in Nazi-occupied France and would release it if the invasion succeeded. In the second, he wanted to shoulder the blame if it didn’t (hence the reason for it never being released).

In the event of a victory, Eisenhower was willing to graciously share the credit. More importantly, in the event of a failure he was willing to unconditionally accept the blame. Eisenhower knew the risks involved with storming Normandy and the rewards for doing so. He knew that in order to pursue such a course of action, he had to take complete ownership of the outcome, regardless of how it unfolded. He had to be prepared for whatever situation followed, especially if the one he hoped for didn’t come to fruition.

Sadly, it feels like we see fewer and fewer people taking these sorts of actions these days. Yet, these are precisely the types of people we need most. Those willing to share the credit and accept the blame. Those with the right amount of confidence.

A Halsted vs. Eisenhower Investor

So, how do you identify an investor with the right amount of confidence? One who is confident in their ability, but also willing to share the credit during good times, accept the blame when things go wrong, seek out disconfirming evidence and opinions, and amend their positions when the facts change? Said another way, how do you differentiate “Halsted investors” from “Eisenhower investors”? It starts with humility and ownership, which manifests itself in an investor’s dollar weighted returns.

Humility and Ownership

When you talk to most investors, their pitch books are filled with examples of their “wins”, “5x returners”, investments that “returned the fund”, and compounders. I get it. If I were in their shoes, I would probably do the same thing. The trouble is, doing so tells very little about what type of an investor they are. Are they cherry picking their winners? Was their success a product of a secular tailwind? Was it more luck than skill? The answer could be one, two, or even all three of these factors.

Now imagine you’re interviewing a different kind of investor. You can’t put your finger on it, but there is something unique about them. You sit down across the table and they hand you their pitchbook. They start going through it. As expected, the investor highlights a few of their winners, their “5x’ers”, and their compounders. Pretty standard stuff. But then they direct you to a few additional pages. You don’t see pages like this very often unless you request them.

The investor is highlighting their mistakes. Cases where things didn’t go as expected. Investments that went sideways, but where they acknowledged their missteps and took actions to address them. They may have started by temporarily reducing the fees they charged their limited partners. If it was a private investment, maybe they chose to dedicate more resources to it, or maybe they saw the writing on the wall and sold it for a loss. If it was a public company, maybe they had to make the difficult choice between doubling down or cutting bait. Maybe they went back to their limited partners to raise additional capital in order to execute a direct financing with favorable terms at a very difficult moment through a private placement.

The potential scenarios are nearly endless, but the point is, like Dwight Eisenhower prior to D-Day, they were willing to preemptively take responsibility and ownership for whatever situations had occurred in their portfolio. By highlighting their wins and their losses, this type of investor is doing the equivalent of “writing two letters.”

The Market Today

With more half of the companies in the NASDAQ down more than 30% from their 52-week highs and a third down more than 50%, many investors are suffering through some pretty abysmal performance for the first time in a decade (or more). More importantly, if these funds had large capital inflows or raised massive vintages in recent years, their dollar weighted returns and IRRs are at risk of looking unfavorable versus their time-weighted-returns.

Today, these investors are undoubtedly experiencing a strong temptation to ignore the current realities, double down on their pre-existing beliefs, take outsized bets to make up for paper losses, or to even begin considering contingency plans in the event that capital flows out as quickly as it flowed in (winding down the fund, diversifying into other funds, converting to a family office, etc.) Unfortunately, we are already beginning to see some of this play out.

Within the public markets, look no further than ARKK Invest. In recent weeks, CEO Cathie Wood has defended the underperformance by blaming other investors for not investing gene editing, electric vehicles, and artificial intelligence and instead focusing too much on benchmarks; a mistake she says could be the “biggest misallocation of capital in the history of mankind”. To no one’s surprise, her fund is exclusively focused on these types of technologies. Or Melvin Capital loading up on Facebook shares in January in a potential attempt to get back over the fund’s high water market after losing billions on his GameStop short (only to see it fall more than 30% in February). Or the countless SPAC investors who lured investors in with the promises of riches, only to leave them with little-to-nothing to show for it.

Within the private markets, we have seen a number of managers raise massive funds at record speeds, new players to the venture game write bigger checks in more rounds in more companies with less diligence, and a massive amount of dollars flow into the crypto space on the belief (and in the hope) that it upends traditional finance.

These investors may in fact end up being right, or maybe they won’t. Time will tell, but either way, their dollar-weighted returns will be the arbiter of the truth.

The Opportunity

Interestingly, this must be a topic on other investors minds because when I opened this weekend’s Wall Street Journal, Jason Zweig had written an article about the exact same topic. In fact, he even used Dwight Eisenhower’s two letters as a framework for his thesis that “since investors natural instinct is to blame others when our portfolios tank, we should write a D-Day note.”

The fact is, while moments like these can be trying, they undoubtedly create an opportunity for investors. An opportunity to define what kind of investors they want to be. To be candid with their partners. To reconstitute discipline if it has waned. To acknowledge missteps. To be prepared to change course if necessary, or communicate effectively the reasons if not. To build a track record that endures as opposed to one attributable to riding a secular wave. To “write two letters” and choose to be an Eisenhower investor.